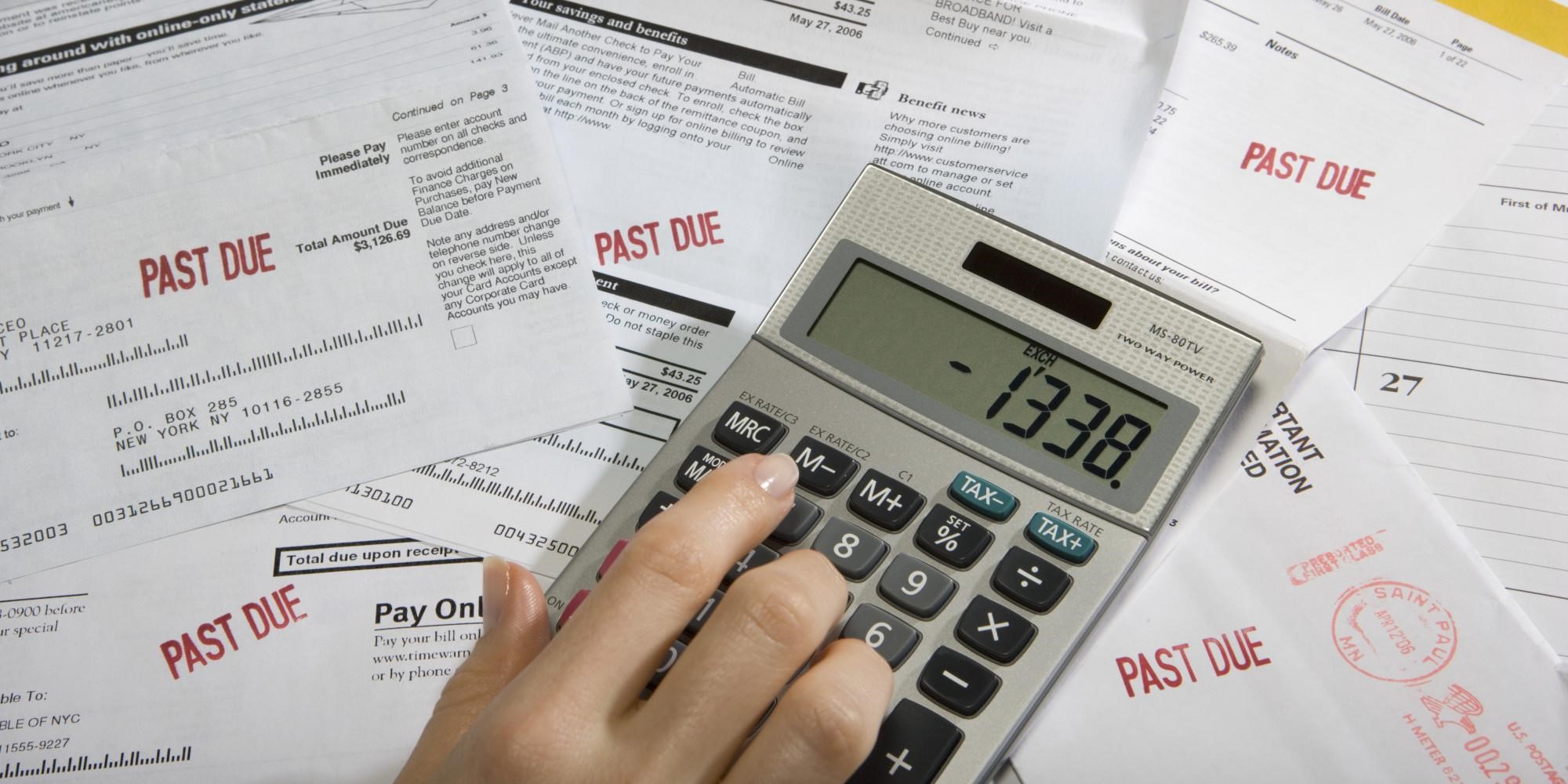

How to Catch up When You Fall Behind on Bills

Paying your bills on time was always a bit tricky. However, in today’s economy, when the majority of people are living from one paycheck to another, falling behind on bills becomes much easier. And once you start falling behind, getting back on the right track becomes very difficult.

Late payment, insufficient funds and overdraft fees, as well as interest, will in no time drain your account and add up to your already increasing credit card balance. So, how can you get back on the right track and pull yourself up from the flooding debt? Here are a few tried and tested ways you can catch up if you’ve fallen behind on your bills.

Make a list

First and foremost, you should make a list of what you owe to figure out how much money you need to put aside each month for the bills. Make sure to note down any payment that’s due, in order to avoid completely forgetting about it. This is particularly important if you have multiple outstanding debts. This list should include everyone you owe money, how much you owe them, how much time do you have to repay them and what the current minimum monthly payment is.

This will help you define where you are currently standing and prioritize when it comes to paying off your debt. It will help you see things clearly and come up with a strategy to move forward. Also, if whoever lent you the money is being impatient or difficult to reach an agreement with, you should try to pay them off first. This will lower your stress levels and protect you from collectors.

Determine your budget

Determining your budget is of vital importance if you want to make sure you have a complete financial picture. In order to be able to determine how much money you can afford to spend, you first need to know exactly how much capital you’re operating with.

With a clear budget in place, you will be able to determine what your priorities are and act accordingly. Even though some people view budgets as restricting, the truth is the exact opposite; meaning, if you have a good budget plan, you will be able to organize your spending more easily.

Work on lowering your expenses

As long as you are behind on your bills, unnecessary expenses should take a back seat. It’s important to understand that yes, those shoes do look amazing, and they will probably make you happy for a while, but another $50 off your budget definitely won’t. Also, try running outside instead on a treadmill and try to work out at home, at least until you sort your finances out.

On the other hand, if you’ve done everything in your power to lower your expenses, but that’s still not enough, don’t despair as there are other options to consider. You can apply for a bank loan, but keep in mind that if you have a bad credit score, banks can deny you the loan or charge you with an extremely high interest rate. That’s why you should apply for bad credit loans instead, because they allow for more freedom and flexibility when it comes to paying them off.

Note down and plan out your daily spending

Having a budget is, as already mentioned, very important. However, no matter how good your budget plan is, it will be practically useless if you don’t keep regular track of your daily spending. Once you determine your overall budget, you should create a daily budget and try to limit your spending.

Here, you should include all of your discretionary spending like groceries, gas money, lunch money, etc., because these expenses are where people usually go off budget. Keep in mind that the $10 spent on gas, even though a necessity, is still $10 less in your budget. On the other hand, since these expenses are not fixed, here is where you can save a few extra bucks. For example, if you drive to work every day, try carpooling and splitting your gas bill with other passengers equally.

Negotiate

If you are falling behind on your bills, you’re not the only one who wants to get back on the right track. Your creditors will also benefit if you make regular payments. Therefore, you should try to negotiate with your creditors and try to come up with a new strategy together. They might lower your interest rates, postpone your due date or waive fees that are preventing you from meeting your monthly obligations.

Before you schedule a meeting with your creditors, however, you will need to check your daily budget to know exactly how much you can afford to spend. Also, you need to let them know how much you are able to spend and what you are able to do, not the other way round. If they are truly interested in helping you out – and they usually are because some money is always better than no money, you will be able to negotiate a better deal.

Falling behind on bills is fairly easy to do, but it can have major consequences for your financial status and long-term plans. If you start falling behind on payments, you should be proactive and deal with it as soon as possible. Otherwise, you may end up in debt you can’t easily repay.

- Top 20 most sought-after vacancies - November 8, 2022

- How to Design an Office for Improved Productivity - April 6, 2022

- Franklin Engineering: Diesel Engine Reconditioners Guide for Business Vehicles - April 6, 2022